Sign up:

Sign up:

Sign up:

Sign up:

Sign up:

Sign up:

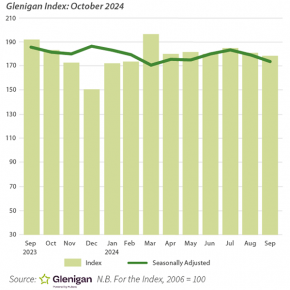

The Index focuses on the three months to the end of September 2024, covering all underlying projects with a total value of £100m or less (unless otherwise indicated, with all figures seasonally adjusted).

It’s a report that provides a detailed and comprehensive analysis of year-on-year construction data, giving built environment professionals a unique insight into sector performance over the last 12 months.

Frustratingly, the October Index sees overall construction industry performance return to a state of stagnation, with declines in residential and non-residential sectors resulting in an overall drop in project starts. Overall, the value of underlying work starting on-site fell 3% against the preceding three months to stand 7% lower than a year ago.

Whilst growth in civil engineering starts represents a slight silver lining in an otherwise disappointing set of results, these positive figures will likely be short-lived as the overall future of major public projects hangs in the balance. It’s further tempered by a generally gloomy short-term outlook for the sector, with poor performance recorded across residential and non-residential verticals, implying tough times ahead in the immediate future.

“Many will be disappointed that the hopes of revival, often heralded by the election of a new Government, have not yet come to fruition. Confidence remains low in the private sector, not helped by the prospect of the upcoming Autumn Budget Statement, which many see sweeping changes to tax and planning policy.

“Investors are, understandably, cautious. Likewise, a lack of clarity on public sector spending has also pushed back project start dates and left some up in the air altogether. Everyone will be on tenterhooks to see what will come out of the Spending Review, but this is still months away and leaving many high and dry. It makes an uncertain situation even more precarious, and the sector is in a delicate position, highlighted by the collapse of ISG and its subsidiaries last month.

“However, the sector has weathered far worse storms than this, and it was encouraging to see Hotel and Leisure starts way up on previous figures, hinting at a much-needed revival in one of the UK’s hardest-hit verticals. Hopefully, clarity on the announcements will help to assuage the unease, which is having a significant knock-on effect on almost every other vertical, dampening overall construction-starts.”

Taking a closer look at the sector verticals and UK regions…

Residential project-starts weakened during the three months to September, however, the impact was softer than earlier this year and less severe when compared to 2022 figures. The value fell by 2% against the preceding three months to stand 9% lower than 2023 levels.

Private housing construction-starts rose by 2% against the preceding three months, experiencing a modest 3% decline on the year before., dropping 3%.

Social housing project-starts suffered, declining 12% against the preceding quarter and 24% compared to last year.

The non-residential sector was more severely affected, posting sharp project-start declines during Q.3.

The one shining beacon was Hotel & Leisure, which experienced a strong period, increasing by 29% against the preceding three months and 83% against the previous year. Strong performance in the sector was boosted by the £34million West Denton Leisure Centre development in Newcastle-Upon-Tyne.

Civil engineering project-starts achieved minor success, performing well against the preceding quarter, increasing 8%. This growth can be largely attributed to the value of infrastructure work starting on-site, which increased 5% against the preceding quarter and by 20% on the previous year. Utilities starts also performed well, increasing 12% against the preceding three months to stand 5% up on last year.

Office project-starts were the biggest loser, with project-starts declining 33% against the preceding three months as well as 37% compared with the year before.

The industrial sector also experienced a torrid Index period, weakening by 21% against the preceding quarter, tumbling 17% on the previous year.

Community & Amenity (-12%) and Education (0%) performance failed to grow against the preceding quarter, both suffering falls of 6% and 9% respectively against the previous year.

Overall, UK regional performance was poor, with most regions suffering declines in project-starts.

The North East and Wales experienced the greatest falls in project-starts against the preceding quarter, cascading 44% and 36%, respectively. Both regions also plummeted on the previous year, declining 39% and 47%.

Yorkshire also performed badly, with project-starts falling 28% against the preceding quarter to stand 16% lower than a year ago.

The value of starts in London declined 9% against the preceding three months and remained 26% down on the previous year.

However, there were a few bright spots. Project-starts in both the South West (+14%) and Northern Ireland (+7%) grew against the preceding three-month period, advancing 13% and 42% against a year ago, respectively.

This was also the case in the East of England, which experienced an increase against both the preceding three months (+8%) and the previous year (+14%).

Passivent has supplied a combination of Hybrid Plus2 Aircool ventilators and Hybrid Plus Airstract roof ventilation terminals for a new London primary school.

Posted in Air Conditioning, Articles, Building Industry News, Building Products & Structures, Building Services, Case Studies, Ceilings, Facility Management & Building Services, Heating, Ventilation and Air Conditioning - HVAC, Restoration & Refurbishment, Retrofit & Renovation, Roofs, Sustainability & Energy Efficiency, Ventilation, Walls

Both a building’s users and its developers have a good reason to get excited about the new Troldtekt Plus 25 panels. This specially developed acoustic panel sets a high standard for both sound absorption and building efficiency.

Posted in Acoustics, Noise & Vibration Control, Articles, Building Industry News, Building Products & Structures, Building Services, Building Systems, Ceilings, Facility Management & Building Services, Floors, Innovations & New Products, Insulation, Interior Design & Construction, Interiors, Restoration & Refurbishment, Retrofit & Renovation, Timber Buildings and Timber Products, Walls

Building on the success of last year, InstallerSHOW is returning to the NEC from the 24th to the 26th of June…

Posted in Articles, Building Industry Events, Building Industry News, Building Products & Structures, Building Services, Exhibitions and Conferences, Health & Safety, Retrofit & Renovation, Seminars, Sustainability & Energy Efficiency

ABLOY, part of ASSA ABLOY Group, has redefined its brand, focusing on the value it brings to customers around the world…

Posted in Access Control & Door Entry Systems, Architectural Ironmongery, Articles, Building Industry News, Building Products & Structures, Building Services, Case Studies, Doors, Facility Management & Building Services, Health & Safety, Retrofit & Renovation, Security and Fire Protection